It’s safe to say Paycom (NYSE:PAYC) investors were not enjoying Wednesday’s market action. Shares are down almost 40%, as of this writing, after the payment software firm delivered a disappointing Q3 report that featured softer-than-anticipated revenue and a subpar Q4 guide.

Revenue in the quarter reached $406 million, and while that represented a 21.5% improvement on the same period a year ago, the figure fell short of Street expectations by $5.06 million. There was better luck at the other end of the equation as adj. EPS of $1.77 climbed from $1.27 in 3Q22 and also outpaced the analysts’ call by $0.16.

However, that was too little for investors who were unhappy about what’s coming next. For Q4, Paycom sees revenue hitting the range between $420-$425 million, some distance below consensus at $452.3 million. Moreover, the company guided for adj. EBITDA of $169-$174 million, while the prognosticators were looking for $189 million.

Lining up to scrutinize the print, analysts were virtually unanimous in pinpointing where the issue lies, placing the blame on the company’s Beti product, which involves employees doing their own payroll and being guided to find and fix errors before payroll submission. Almost two-thirds of Paycom’s clients have shifted to Beti, management said during the company’s earnings call.

That thesis is one TD Cowen analyst Bryan Bergin agrees with. “Rising Beti usage is leading to revenue cannibalization as the amount of off-cycle payroll runs & services revenue associated w/ correcting errors are being eliminated,” Bergin said. “While this is clearly a cost savings benefit to clients — PAYC is leaning into a message of fundamentally changing the industry via greater efficiency — it’s a notable revenue headwind and puts PAYC on an initial FY24 growth view that’s close to COVID lows. Cross-sell activity also remains muted while PAYC remains focused on driving Beti adoption through its base; nearly two-thirds of clients on Beti, up from 60% in 2Q.”

In the face of increasingly difficult times and during a period of transition, Bergin anticipates that more transparency will be crucial to bolster investor confidence in a recovery. “PAYC’s strong & consistent performance before made this less of an issue,” Bergin went on to add. “However, this may need to change.”

Meanwhile, the weak results are why Bergin has downgraded his PAYC rating from Outperform (i.e., Buy) to Market Perform (i.e., Neutral). Additionally, the price target is lowered from $331 to $202. Nevertheless, there’s still upside of 33.5% from current levels. (Watch Bergin’s track record)

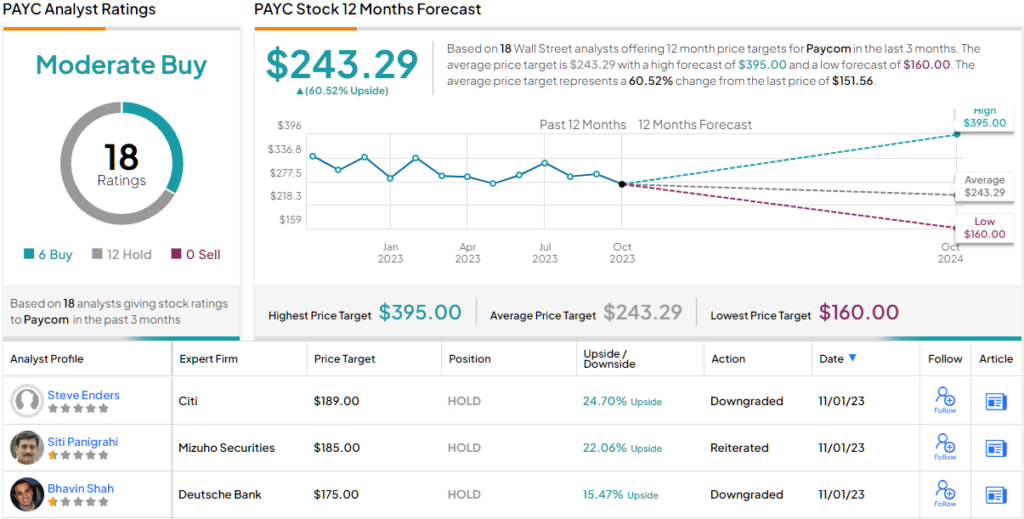

So, that’s TD Cowen’s view, let’s turn our attention now to rest of the Street: PAYC’s 6 Buys and 12 Holds coalesce into a Moderate Buy rating. Following the share price meltdown, there’s plenty of upside in store; according to the $243.29 average target, investors will be pocketing gains of 60% a year from now. (See Paycom stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.