SweetBunFactory

Introduction

ASML Holding (NASDAQ:ASML) is one of the leading companies in the semiconductor sector, playing a crucial role in the industry. Its stock performance history has been extraordinary, with a notable increase of 380% in the last five years. Despite these successes, there have been signs of uncertainty regarding its long-term potential.

Some recent news raises doubts about the sustainability of ASML's EUV technology, especially in the face of competition from Japanese companies such as Canon. Additionally, the issuance of a less optimistic guidance for the year 2024 has raised additional concerns about the company.

From my perspective, the competition from Japanese companies does not seem to significantly threaten ASML's dominant position in the market. On the other hand, although the guidance for the current year may appear poor, I maintain the conviction that the company's future remains promising in the long term. In this article, I will explain the reasons why I believe these apparent risks may not be as alarming as the news suggests.

How ASML's EUV Machine Works

First, before explaining why I believe Canon and Nikon don’t put at risk ASML's monopoly in EUV, I think it's important to understand, not too in-depth, as I don't consider myself an expert in this field, how ASML's EUV machine operates.

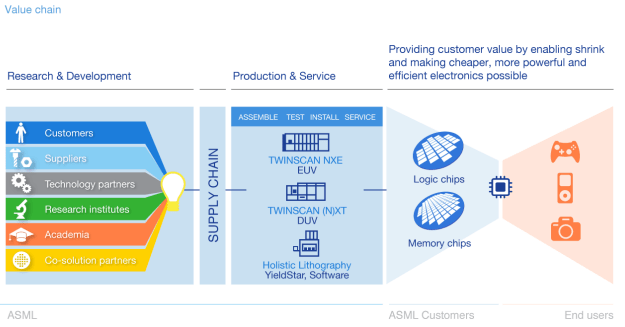

ASML Investor Relations

ASML's EUV machine uses an extreme ultraviolet light source to project circuit patterns onto a silicon wafer. This light source is generated through a plasma process where a high-energy laser is used to heat and vaporize a material called tin. The vaporized tin emits extreme ultraviolet light, which is then focused and directed onto the silicon wafer.

The pattern projection onto the silicon wafer is achieved through a system of high-precision mirrors and lenses. These optical components enable the extreme ultraviolet light to be focused with extremely high resolution, allowing for the creation of microscopic circuits on the wafer.

One key feature of ASML's EUV machine is its ability to project patterns with a much shorter wavelength than previous technologies. This enables higher resolution and precision in chip manufacturing, consequently allowing for the creation of smaller and denser circuits. This capability is essential for continuing to advance Moore's Law, which posits that the number of transistors on a chip roughly doubles every two years.

In addition to its high-resolution pattern projection capability, ASML's EUV machine also provides higher energy efficiency compared to previous technologies. This is partly due to the use of extreme ultraviolet light, which enables greater precision in pattern projection and reduces the need for additional processing stages.

The Greatest Moat of ASML

When discussing ASML and why it is so challenging to replicate its technology, analyses often focus on the extreme complexity of the EUV machine, attributing the difficulty for competitors to replicate it. While this is undoubtedly true, I believe there is an even more crucial reason why I think it is nearly impossible for any competitor worldwide to replicate ASML's technology, and that is its supply chain. In fact, in the words of Frits Van Hoyts, who took the reins of the EUV project in 2013, the key to developing the EUV machine was not any specific breakthrough but ASML's ability to manage its supply chain.

ASML 10K

In the early stages of machine development, ASML only manufactured 15% of the EUV machine components; the rest had to be sourced from thousands of external suppliers, yes, thousands. One might consider this a weakness for ASML. If several suppliers failed, it would be completely incapacitated for the production of new units. However, I believe this is not the case.

Most companies, especially those crucial to the supply chain, have exclusivity contracts signed with ASML. This means that even if someone outside of these companies wished to acquire their products to attempt replicating their technology, they couldn't do so and would be forced to seek alternative suppliers. This, evidently, proves to be a quite challenging task, especially considering the type of product we are discussing.

Furthermore, ASML holds such a strong dominance in this supply chain that if it sees any of its suppliers not meeting expectations, it can simply acquire them. This is not mere speculation; it has already happened. ASML acquired Cymer in 2013, HMI in 2016, or Berliner Glas Group in 2020, among other companies involved in its supply chain. These companies are typically much smaller than ASML, allowing ASML to acquire them relatively easily if they believe that their supply chain is at risk or if they think they can do better by leading the companies themselves.

Manufacturing the world's most complex machine requires one of the most complex supply chains, and ASML has almost complete control over what happens in them, thanks to its exclusivity contracts and its ability to acquire key players in the supply chain. For any competitor attempting to replicate its technology, in addition to the exceedingly difficult task of copying its intellectual property, they must also be capable of establishing and controlling a similarly challenging supply chain. This is something that seems practically impossible to me, at least in the short term, considering the current position of its closest competitors, in my opinion, Canon and Nikon.

Why ASML Will Win in EUV?

Even though we've established that ASML's technology is highly challenging to replicate due to its complexity and intricate supply chain, there's an additional reason that leads me to believe ASML will prevail in the field of EUV. Let's consider the worst-case scenario: one of its competitors manages to replicate its technology and brings a machine with the same capabilities to the market. Given the limited number of customers in the market, how would they displace ASML?

Currently, the world's most significant semiconductor foundries have their backlogs based on ASML's technology. ASML is a reliable supplier for them, providing cutting-edge technology and proving to be highly profitable. I highly doubt they would want to switch suppliers, considering all the potential problems this could cause. It would essentially mean abandoning a production standard that has been working for decades for another that, at best, will provide similar results but introduces a significant risk that the transition to the new supplier may not be successful.

Therefore, to incentivize major clients like Samsung (OTCPK:SSNLF) or TSMC (TSM) to switch their primary supplier, you not only need to match ASML in performance and price but also surpass it. Considering how improbable it seems for them to match ASML's technology, the idea of someone surpassing it by a significant margin appears almost impossible. Especially when we take into account that ASML is the leading investor in research to develop the next generation of its technology. In the past year alone, they invested €4bn in R&D, and they anticipate investing over €6 billion by 2030. If someone were to surpass ASML's technology, it seems that it would be ASML itself.

What I've just mentioned has already occurred in the history of semiconductors. In Chris Miller's book "Chips War" there's a chapter dedicated to GCA, an American semiconductor manufacturing equipment company very similar to ASML today. This company fell behind in developing cutting-edge technology, and when it tried to catch up, it was simply too late. Customers had already become accustomed to using equipment from competitors and disregarded GCA's technology, even though, according to some industry insiders, it was superior.

"The software used by GCA's machines was far superior to that of the Japanese competition. A lithography expert from TI who tested GCA's latest machines acknowledged this: 'They were ahead of their time.' (...) Customers had already become accustomed to equipment from competitors such as Nikon, Canon, and ASML. They were not willing to take risks with new and unfamiliar devices from a company with an uncertain future. If GCA went bankrupt, customers might face difficulties finding spare parts. Unless a major client could be convinced to sign a significant contract with GCA, the company would spiral into negativity until disappearing." - Chips War, Chris Miller.

This is just one example of several times such events have occurred throughout history. Moreover, the current market is much more consolidated than it was in the 1980s, so I believe this effect would be even more pronounced. On the other hand, the longer ASML remains a monopoly in the field with its EUV machines, the more accustomed its customers will become to its technology, making it increasingly challenging for them to switch to another competitor's technology.

Lastly, I find it interesting to note that the three main customers and chip manufacturers for ASML today—Samsung, Intel (INTC), and TSMC—invested significant sums of money in ASML during the development of EUV technology. Therefore, it is logical to assume that they would prefer to use the technology in which they invested their capital for development. While it's true that Samsung has been divesting its investments in ASML, I consider this point the least relevant in this context.

Guidance for 2024 is weak

In the latest earnings presentation, ASML mentioned that they expect sales in 2024 to remain virtually flat. This alarmed many investors, as ASML is consistently categorized as a 'growth' company, and how is it possible for a growth company not to grow?

Seeking Alpha

The clear answer to this lies in the fact that, as we've discussed, the semiconductor market is a cyclical industry. When demand increases, manufacturing capacity also increases, as seen post-pandemic in 2020 and 2021. Currently, demand has decreased, leading chip manufacturers to postpone some of their investments in capacity expansion. However, demand will rise again, as it has been happening since the inception of the sector and will continue for many more years as long as the sector's tailwinds (cloud, digitization, 5G, IoT, etc.) persist.

Therefore, I don't believe that this lower guidance for the next year reflects a deterioration in their business or a lack of interest in their technology. Instead, it more accurately mirrors the cyclical nature of the industry. In fact, some executives from TSMC and ASML themselves stated in recent earnings reports that they believe the bottom of the cycle is very close or that we might already be in it. Indeed, 2025 is anticipated to be a year of significant growth for the sector overall and for ASML in particular. ASML's CEO himself stated the following:

“We therefore expect 2024 to be a transition year. Based on our current perspective, we take a more conservative view and expect a revenue number similar to 2023. But we also look at 2024 as an important year to prepare for significant growth that we expect for 2025.” - ASML President and Chief Executive Officer Peter Wennink.

From my perspective, we shouldn't view 2024 as a year of weakness for ASML but rather one of strength. If, in the trough of the cycle, your sales remain flat, it's a significant success in my view. Considering that companies like Intel, AMD (AMD), Texas Instruments (TXN), or Analog Devices (ADI) have seen declines in their sales in recent quarters, seeing ASML maintain the same revenue level demonstrates that its moat remains very strong.

I understand that some investors prefer to see two consecutive years of 10% growth instead of one year at 0% and the next at 22%. However, the semiconductor industry has operated this way for decades and is likely to continue doing so. The best approach for us as investors is to be aware of this and take advantage of the potential market volatility resulting from the abrupt changes in expectations that often occur.

My outlook for the coming years

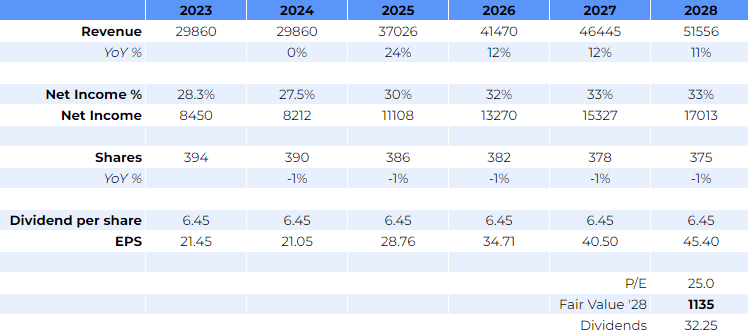

So, how do I think this will translate into numbers in the coming years? I have formulated this projection for the upcoming years based on my expectations regarding ASML's outcomes.

As we have already explained, I believe that 2024 will be a transitional year, so I have projected no growth in the top line, and consequently, the margin will depress slightly. However, in 2025, as stated by the management, growth is expected to return, and I have projected a 24% increase in the top line with a notable margin expansion. From then on, I believe that growth will moderate to more sustainable double-digit rates, while the margin continues to expand slightly.

On the other hand, I think there will continue to be share buybacks due to the significant amount of cash flowing into the company. We have already seen that they expect to reach around €6bn in R&D annually, and capex will be around €1.5bn according to their own estimates. Therefore, the amount of excess cash will be substantial, and I believe they will choose to return it to shareholders in the form of share buybacks. I have projected a 1% annual decrease in outstanding shares. Additionally, to calculate the total return on our investment, we must consider that ASML pays a small dividend of around a 1% yield. To be extremely conservative, I will assume that this will not grow in the coming years, although the possibility of this happening is really low.

Author's Calculations

With all these data, and applying a final multiple of 25x, which, considering the quality of this business, seems appropriate to me, we obtain a valuation for 2028 of $1031 per share. This leaves us with a potential compounded annual gain of 10% until 2028, without taking into account the dividend; if we consider it, it would be 11%.

As we can see, the prospects for 2024 are not the best; however, if we extend our view beyond that, we see that the long-term potential for ASML remains enormous. Personally, I am trying to buy it below $680, but since an 11% annual return already seems acceptable to me, I am going to give ASML's stock a hold rating.