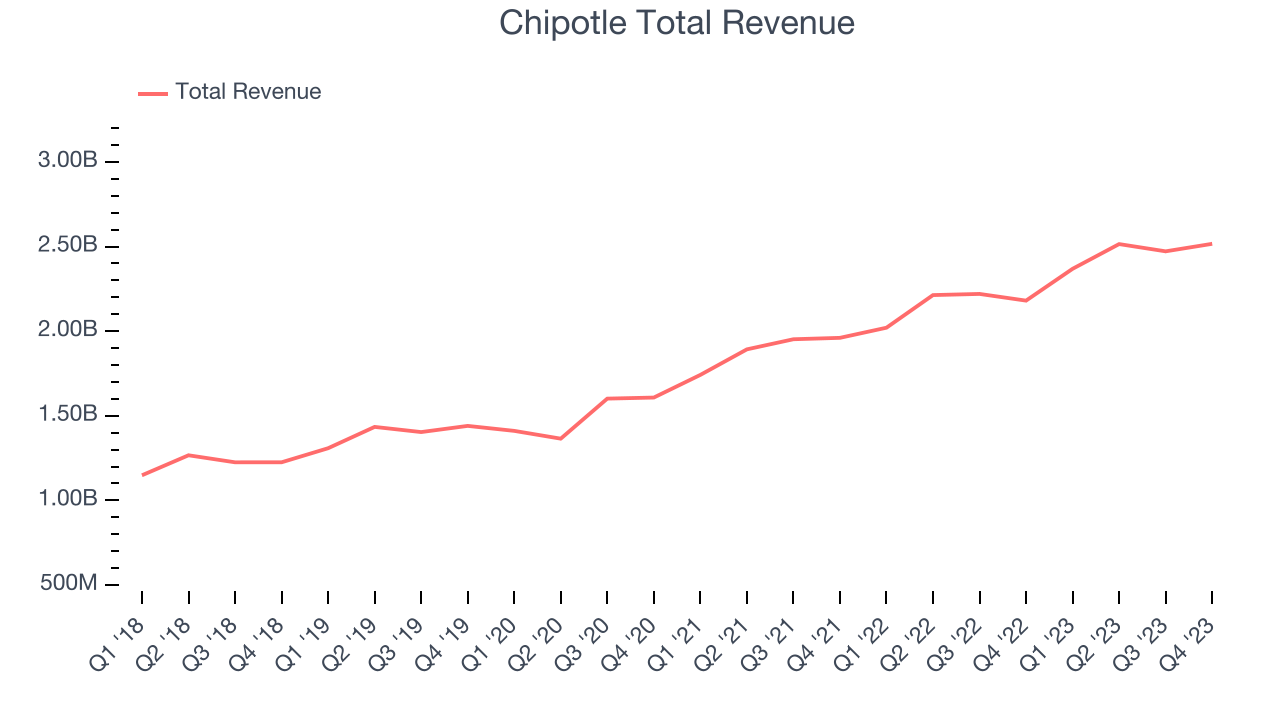

Mexican fast-food chain Chipotle (NYSE:CMG) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 15.4% year on year to $2.52 billion. It made a non-GAAP profit of $10.36 per share, improving from its profit of $8.29 per share in the same quarter last year.

Is now the time to buy Chipotle? Find out by accessing our full research report, it's free.

Chipotle (CMG) Q4 FY2023 Highlights:

- Revenue: $2.52 billion vs analyst estimates of $2.49 billion (1.1% beat)

- EPS (non-GAAP): $10.36 vs analyst estimates of $9.73 (6.5% beat)

- Free Cash Flow of $93.53 million, down 73.2% from the previous quarter

- Gross Margin (GAAP): 40.1%, up from 39.6% in the same quarter last year

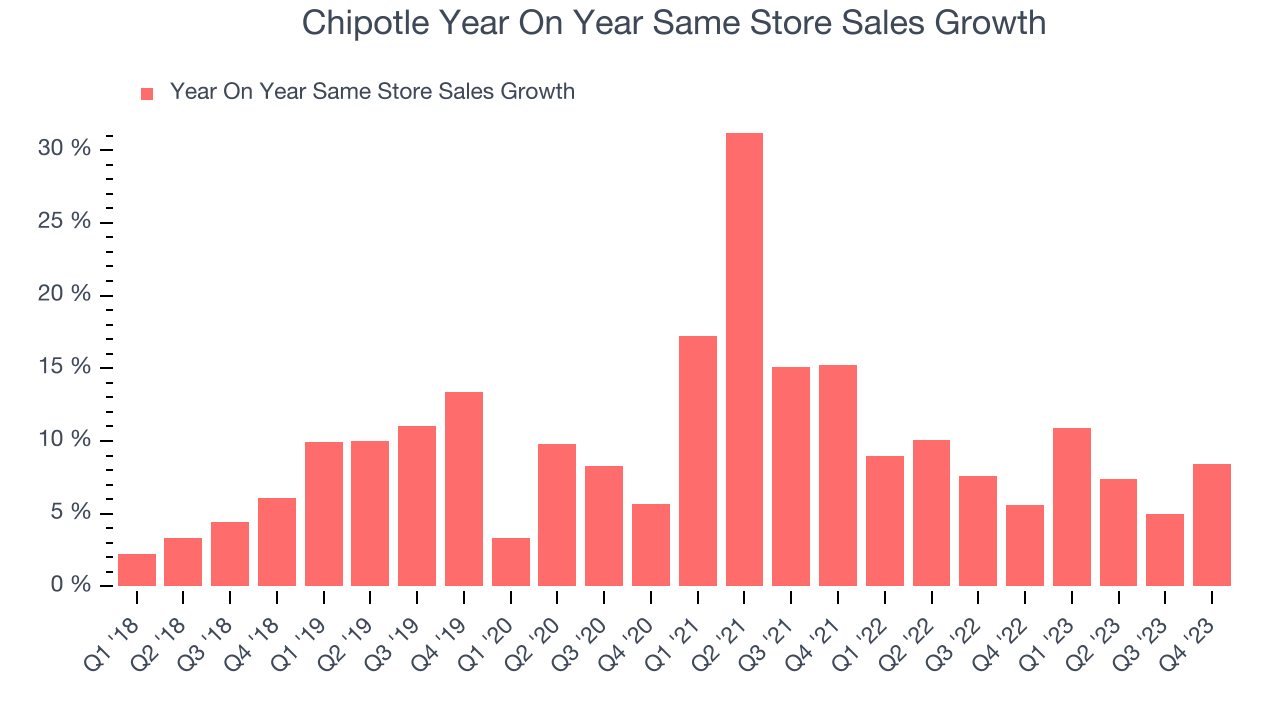

- Same-Store Sales were up 8.4% year on year

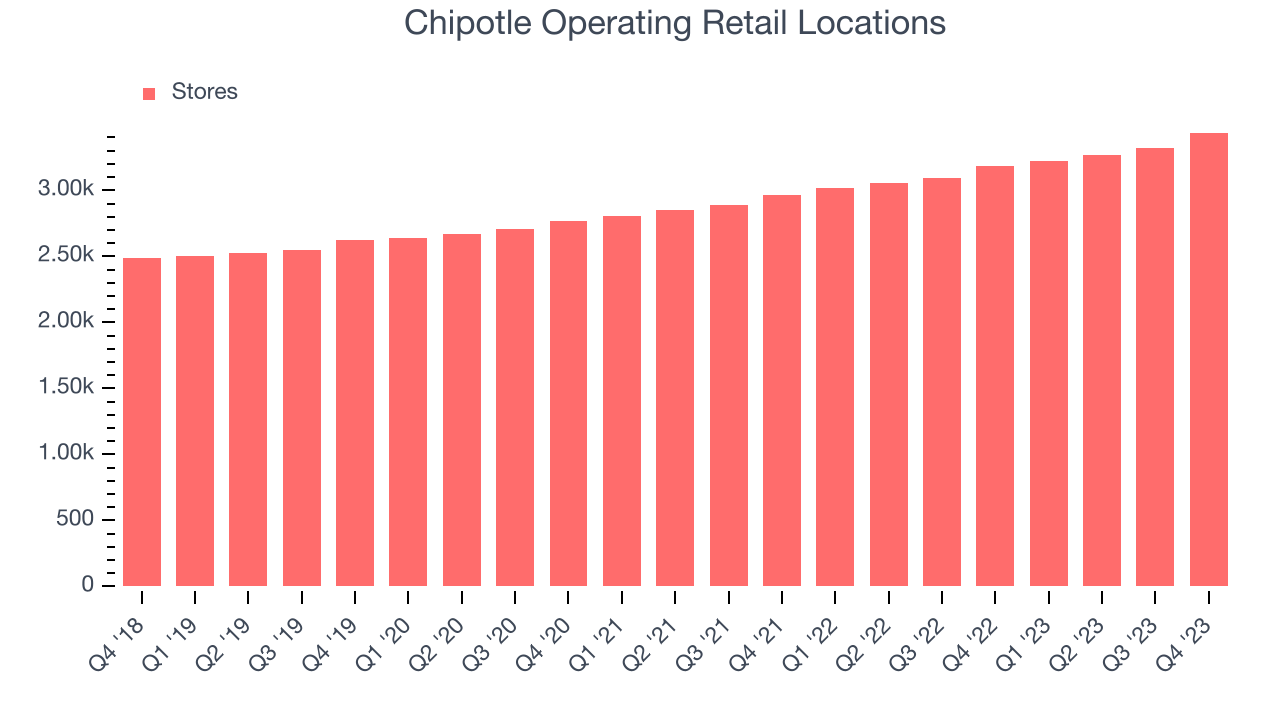

- Store Locations: 3,437 at quarter end, increasing by 250 over the last 12 months

- Market Capitalization: $67.81 billion

"2023 was an outstanding year where we delivered strong transaction growth driven by throughput and menu innovation, opened a record number of new restaurants, surpassed $3 million in AUVs and formed our first international partnership," said Brian Niccol, Chairman and CEO, Chipotle.

Born from a desire to offer quick meals with fresh, flavorful ingredients, Chipotle (NYSE:CMG) is a fast-food chain known for its healthy, Mexican-inspired cuisine and customizable dishes.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

Chipotle is one of the most widely recognized restaurant chains in the world and benefits from brand equity, giving it customer loyalty and more influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 15.3% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it added more dining locations and increased sales at existing, established restaurants.

This quarter, Chipotle reported robust year-on-year revenue growth of 15.4%, and its $2.52 billion in revenue exceeded Wall Street's estimates by 1.1%. Looking ahead, Wall Street expects sales to grow 13% over the next 12 months, a deceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Number of Stores

A restaurant chain's total number of dining locations is a crucial factor influencing how much it can sell and how quickly company-level sales can grow.

When a chain like Chipotle is opening new restaurants, it usually means it's investing for growth because there's healthy demand for its meals and there are markets where the concept has few or no locations. Since last year, Chipotle's restaurant count increased by 250, or 7.8%, to 3,437 locations in the most recently reported quarter.

Taking a step back, Chipotle has rapidly opened new restaurants over the last eight quarters, averaging 7.3% annual increases in new locations. This growth is much higher than other restaurant businesses. Analyzing a restaurant's location growth is important because expansion means Chipotle has more opportunities to feed customers and generate sales.

Same-Store Sales

Same-store sales growth is an important metric that tracks organic growth and demand for a restaurant's established locations.

Chipotle's demand within its existing restaurants has generally risen over the last two years but lagged behind the broader sector. On average, the company's same-store sales have grown by 8% year on year. With positive same-store sales growth amid an increasing number of restaurants, Chipotle is reaching more diners and growing sales.

In the latest quarter, Chipotle's same-store sales rose 8.4% year on year. This growth was an acceleration from the 5.6% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Chipotle's Q4 Results

We enjoyed seeing Chipotle beat analysts' revenue, same-store sales, and EPS estimates this quarter. The company's outperformance was driven by strong year-on-year unit growth of 7.4%. It also got a pricing tailwind of 1.0% and opened more restaurants in the quarter than expected (121 vs estimates of 117). A highlight of Chipotle's 2023 was that it formed its first international partnership with franchisee Alshaya Group in the Middle East. Looking ahead, Chipotle expects same-store sales growth in the mid-single digits for 2024 along with 300 new store openings. We think this was a fantastic quarter that should have shareholders cheering. The stock is up 2.1% after reporting and currently trades at $2,546 per share.

Chipotle may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.