Bill Diodato/DigitalVision via Getty Images

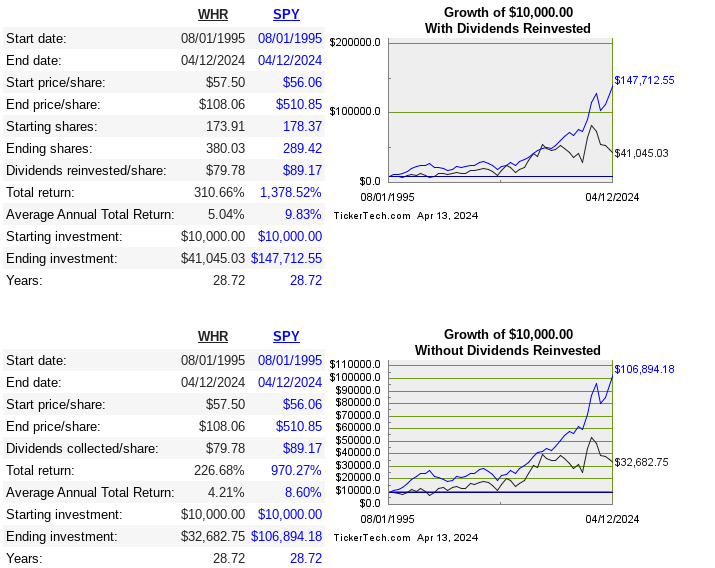

Whirlpool Corporation (NYSE:WHR) is an American manufacturer of home appliances worldwide. They own well-known brands such as Maytag, KitchenAid, and many others along with the main Whirlpool brand. Below are the long-term returns:

dividend channel

Let's see how revenue breaks down across segments and geographies:

WHR 10-K

They operate in many different countries, but North America makes up the majority of sales.

QHR 10-K

Next, let's take a look at their return metrics vs. peers. Keep in mind, Samsung is a peer that derives most of its revenue from different industries entirely, so it's not a pure competitor:

Company | 10-Year Revenue CAGR | 10-Year Median ROE | 10-Year Median ROIC | 10-Year EPS CAGR | 10-Year FCF CAGR |

WHR | 0.4% | 14.6% | 7.1% | -1.6% | -6.1% |

5.5% | 16.4% | 19.1% | 9.5% | 7.7% | |

-2% | 9% | 5.7% | n/a | 1.1% | |

9.9% | 15.1% | 9.1% | 7.1% | 9.9% | |

-2.4% | 15.4% | 9.5% | n/a | n/a |

Capital Allocation

Let's take a look at where capital was allocated over the past decade, in USD millions:

Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

EBIT | 1,324 | 1,443 | 1,541 | 1,411 | 1,273 | 1,300 | 1,903 | 2,281 | 1,218 | 1,137 |

FCF | 759 | 536 | 543 | 580 | 639 | 698 | 1,090 | 1,651 | 820 | 366 |

CAPEX | 720 | 689 | 660 | 684 | 590 | 532 | 410 | 525 | 570 | 549 |

Dividends | 224 | 269 | 294 | 312 | 306 | 305 | 311 | 338 | 390 | 384 |

Repurchases | 212 | 499 | 716 | 1,136 | 140 | 77 | 965 | 900 | ||

Debt Repayment | 606 | 283 | 522 | 564 | 386 | 949 | 569 | 300 | 300 | 750 |

Acquisitions | 1,809 | 439 | 3,075 | 14 |

This is a case where capital allocation is treated too much like a salad bar. A little of this, some of that, a heaping pile of the other thing. Cash flow is to be treated seriously. On a basic level, run the calculation roughly in your head; how can you create value by paying dividends, buying back shares, perpetually paying down debt but also adding debt, and making the occasional acquisition?

It's obvious why it's easier to analyze a company that has a more singular approach, like a roll up company that relies on M&A as the core driver, or a dividend-centric strategy etc.

I would be fine with pulling all of these levers if the end result was consistent wealth creation for shareholders, but the stock is down over past 5 years and barely up at all over 10 years. I actually think this is a case where shareholders would benefit the most from an all-in focus on buying back shares. There is an extensive history of dividends, and cutting it would upset an important shareholder base, but my opinion is that most of the earnings would be best suited to reducing share count and taking advantage of the low multiples. The debt levels must also be addressed, which makes this share cannibal strategy less viable.

The CEO has been in place since 2017, and has been with the company since 2000. I don't expect any major change in capital allocation in the future.

Q1 Earnings

Next, let's take a look and earnings history and upcoming earnings:

Seeking Alpha

I expect another beat next quarter, but I think the longer-term prospects are questionable due to the recent acquisition and overall growth levels more on that in the risk and valuation sections.

Risk

As a brand, WHR is intact over the longer term. This doesn't mean it has brand power in the same manner of a AAPL or NKE for example, where customers are happy to buy a perceived premium product at a premium price. The risk is subpar business performance, which would lead to subpar share performance.

The InSinkErator acquisition was the right kind to make, but the problem is the increased leverage to make the purchase. Long-term debt isn't so big that it will take down the company, but it's at higher levels than I would generally like to see.

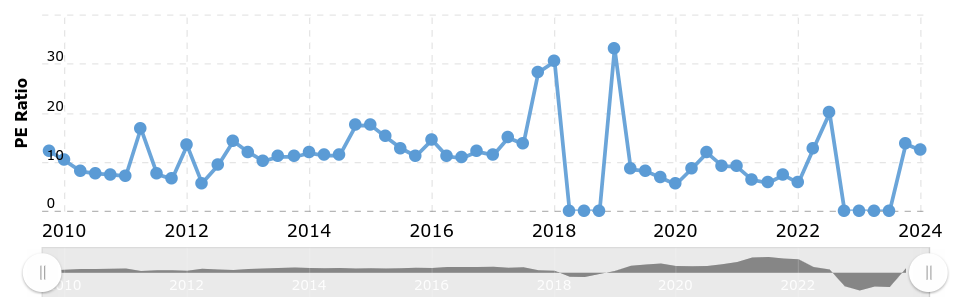

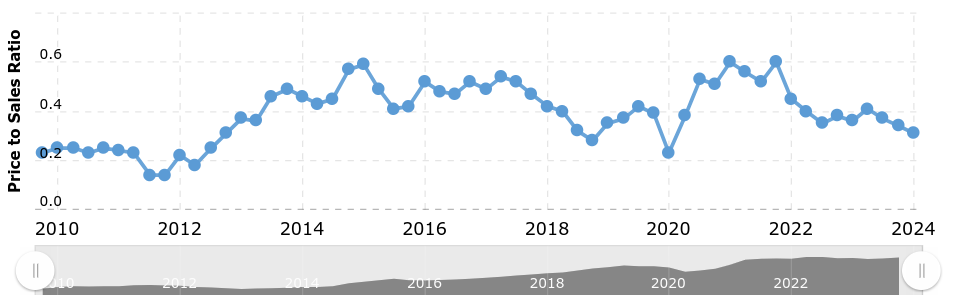

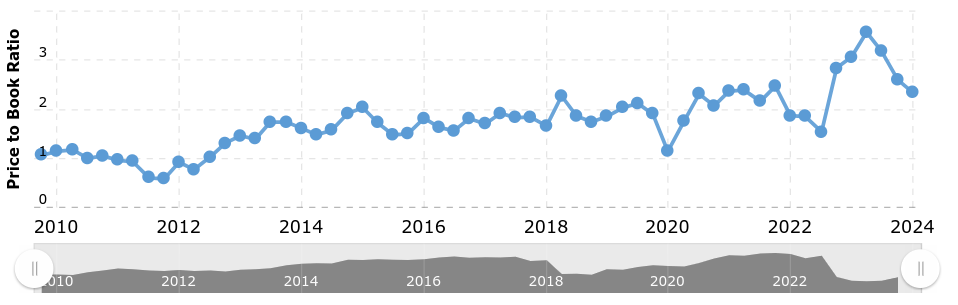

Valuation

WHR's revenue peaked back in 2017, and share prices peaked in 2021. Share prices are currently down almost 60% since then. Let's look at the historical multiples, followed by comparing multiples with peers:

Macrotrends Macrotrends Macrotrends

Company | EV/Sales | EV/EBITDA | EV/FCF | P/B | Div Yield |

WHR | 0.6 | 7.2 | 29.3 | 2.3 | 6.4% |

SSNLF | 1.1 | 4.6 | 12.7 | 1.1 | 2.2% |

PCRFY | 0.4 | 4 | 7.9 | 0.7 | 2.5% |

HSHCY | 0.7 | 7.3 | 12.4 | 2.2 | 2.5% |

ELUXY | 0.3 | 14.3 | -21. | 2 | n/a |

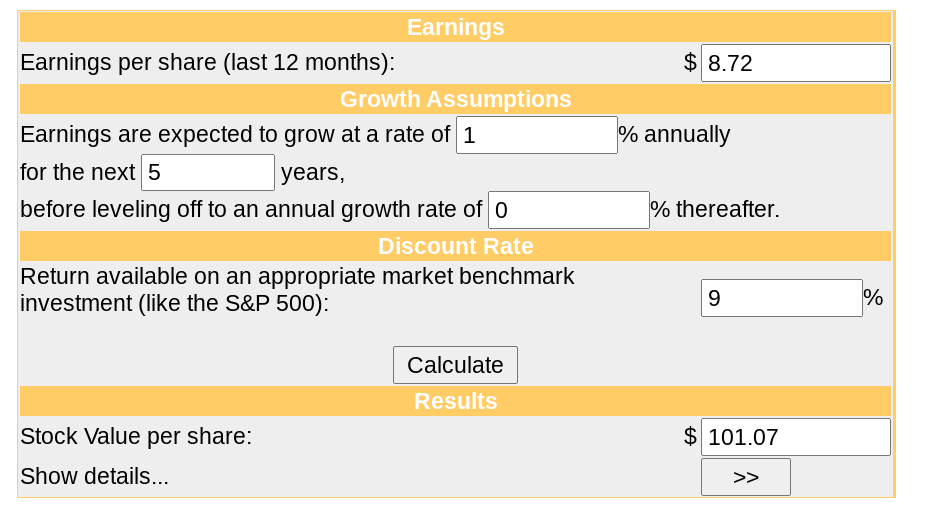

This is another case where the multiple looks low initially, but when we zoom out, we see the rest of the industry isn't far off. There's no indication of cheapness from the multiples, so next is the DCF model:

money chimp

So according to my estimates, it is slightly overvalued today. I've given a conservative forecast of earnings growth, but WHR is the epitome of a mature, blue-chip company that is lucky to grow at the rate of the economy at this point. The 6% dividend yield may look enticing to some, but it could likely be the only return as part of total return.

I wouldn't call this a dividend trap because the risk of the dividend being cut is very low. They've paid a dividend for 68 consecutive years. I also wouldn't call this a value trap because shares aren't plummeting perpetually, which would lead to trying to catch a falling knife. I'm simply saying that the dividend yield might lead investors to believe in a much greater upside than what really exists. I do, however, think the dividend is safe, so if you are looking for a purely "dividend stock", then this could have some interest to you, but why not at least some capital gains to go with it?

To sum up my view, the potential upside of earnings growth from the latest acquisition isn't worth the debt levels taken on to make the acquisition. The stock looks somewhat cheap now mostly because of how much shares have come down since the "peak everything" craze of 2021, which has driven up the dividend yield too. My rating for this stock is "Sell".

Conclusion

WHR has been a major player in the industry for a long time now, and that won't be changing anytime soon. Their most recent acquisition of InSinkErator, purchased from EMR, took debt levels higher, and gives me reasonable concern. When it comes to capital allocation, they do a little bit of everything, and the result has not been a high performing stock.

The 6% dividend might signal undervaluation to some, but this isn't the case intrinsically or when the multiples are compared to the rest of the industry. I don't anticipate any major drawdown, WHR is not a bad company at all. The problem is: Growth is stagnant, so you are essentially getting a 6% bond with no capital gains at all.