Makhbubakhon Ismatova

The recent tech-fueled rally is reminiscent of the FOMO-mentality a couple of years ago, when everyone was trying to get in on the action around meme stocks. This time is different, however, as it's on a much grander scale due to the sheer size of the companies such as Nvidia (NVDA), which has led to whole indices such as the S&P 500 (SPY) and Nasdaq being pulled up.

At the same time, many value stocks have been left in the dust, creating opportunities for bargain seekers who prize income over capital gains. While it may be nice to see unrealized gains on paper, one would have to sell the stock to realize it, and that can lead to more FOMO if said stock continues to shoot higher in the short term.

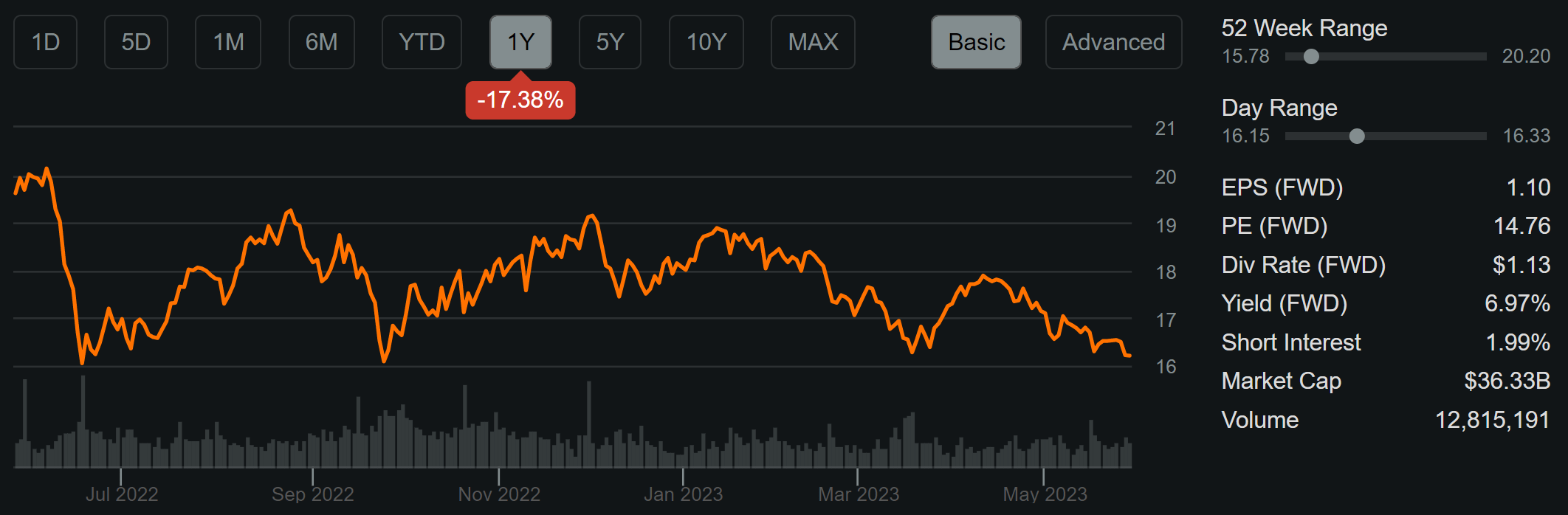

That's why some investors may prefer to buy and hold quality value stocks that throw off decent income, and which they don't have to worry about selling at the right time. This brings me to Kinder Morgan (NYSE:KMI), which, as shown below, is now trading just shy of its 52-week low, while throwing off a 7% yield at the same time.

I last covered the stock here back in March, noting its excess cash flows that gives it financial flexibility. This article highlights recent updates and why KMI is a high income bargain at present.

KMI Stock (Seeking Alpha)

Why KMI?

Kinder Morgan is one of the largest North American energy midstream companies. Its natural gas pipeline network spans 70,000 miles and moves around 40% of U.S. natural gas production. It also has 700 billion cubic feet of natural gas storage, which comprises 15% of the total natural gas storage capacity in the U.S.

Most investors in this industry know that regulatory hurdles have made it more difficult to build fossil fuel infrastructure, including pipelines, in the U.S. That actually makes KMI's existing pipelines more valuable due to reduced competition, and puts the company in a favorable position when customer contracts are up for renewal.

Plus, natural gas will be needed for a very long time, especially considering the recent push by the EPA, which could result in two-thirds of car and light-truck sales to be battery-powered vehicles by the year 2032. With the current electric grid in certain parts of the country that perennially show strain during peak summer weather, relying solely on renewable energy to "plug" the gap simply won't be enough.

As such, natural gas should be ever more important as a means to fulfill ambitious EV ambitions by the current U.S. administration. This is also supported by recent the recent IEA World Energy Outlook, which predicts that fossil fuels will supply 62% of the world's energy demand in 2050, and the U.S. Assistant Secretary of Energy recently stated last month that "the world absolutely needs new gas investment."

Moreover, KMI is also hedging its bets, as 86% of its project backlog is devoted to lower-carbon energy services. This includes RNG (renewable natural gas) and renewable diesel projects, including a new renewable feedstock storage and logistics hub at KMI's Louisiana facility.

Notably, KMI's entire project backlog equates to $3.7 billion, of which $3.3 billion carries an attractive project cost to EBITDA multiple of 3.5x. This is also supported by a strong BBB-rated balance sheet with a net debt to EBITDA of 4.1x, sitting below the 4.5x level generally considered to be safe by ratings agencies.

Meanwhile, KMI is seeing strong transport volumes, which grew by 3% YoY during the first quarter. This was driven by the return of one of its service lines and a 10% increase in deliveries to power plants as a result of colder weather.

While distributable cash flow per share was down by 5% YoY To $0.61, it still amply covered the dividend, which recently grew by 2%, at a 2.16x dividend coverage ratio. It's worth mentioning that the first quarter is traditionally strong for DCF due to winter temperatures, and full year DCF to dividend coverage is expected to land at 1.88x, based on 2023 DCF/share guidance of $2.13.

Lastly, KMI appears to be trading at an attractive discount at the current price of $16.21 with a 7% yield and price to cash flow of just 6.97x, sitting towards the low end of its range over the past 5 years, as shown below. Sell side analysts who follow the company have an average price target of $20.13, implying a potential 24% return based on price appreciation alone.

Seeking Alpha

Investor Takeaway

Kinder Morgan is an attractive midstream energy bargain at present, with a wide-reaching asset base that's ever more valuable due to less new competition. Its natural gas infrastructure is a mission-critical component to a growing EV future, and it's also playing its cards right by investing in lower-carbon energy services and locking in attractive expected returns on projects. With a strong balance sheet, generous dividend yield, and low valuation, value investors ought to give KMI a hard look at its currently discounted price.

Gen Alpha Teams Up With Income Builder

Gen Alpha has teamed up with Hoya Capital to launch the premier income-focused investing service on Seeking Alpha. Members receive complete early access to our articles along with exclusive income-focused model portfolios and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%.

Whether your focus is High Yield or Dividend Growth, we’ve got you covered with actionable investment research focusing on real income-producing asset classes that offer potential diversification, monthly income, capital appreciation, and inflation hedging. Start A Free 2-Week Trial Today!