In a move that resonates with a resounding “take that” to the skeptics, Altria Group (NYSE: MO) has silenced the bears once again as it boldly announced yet another dividend increase. The tobacco giant remains undaunted despite enduring persistent downward pressure on its shares for years. Also, despite Wall Street’s hesitance to align with its “anti-ESG” business model, Altria consistently delivers exceptional financial performance and robust capital returns. Hence, I am bullish on Altria stock.

Dividend Growth Supported by Rock-Solid Financials

On Thursday, Altria announced a 4.3% increase to its quarterly dividend, marking its 54th consecutive annual dividend hike. The company’s dividend growth is supported by strong underlying financials despite the market’s skepticism towards its overall prospects. This was once again verified in the company’s most recent Q2 results, with revenues coming in robust and EPS marking further growth.

To be more precise, in its most recent earnings report, Altria demonstrated strong sales, defying the prevailing narrative of its imminent extinction. In Q2, the company generated net revenues of $6.51 billion, implying a marginal 0.5% decline compared to the previous year’s period. This small dip in net revenues can be attributed to 8.7% lower shipment volumes in smokable products, although much of this decline was counterbalanced by Altria’s adoption of higher pricing.

In my view, despite the broader trend of declining smokeable product sales, the actual scenario is far from the catastrophic portrayal often projected by the market. While relying on escalating prices to offset cigarette demand is not a sustainable long-term approach, I believe that there will always be a segment of the population that continues to smoke. This suggests that there should be a certain threshold at which Altria’s shipment volumes stabilize, mitigating the necessity for frequent price adjustments.

Additionally, an interesting aspect of Altria’s report regarding its smokable segment is that the company is seeing great success in its Cigars division, where shipment volumes actually rose by 7.6%. Considering the growing market appeal of cigars attributed to their image of exclusivity and enjoyment, in contrast to the negative perception often associated with cigarettes, cigars could contribute to the company’s growth in the future.

Record Profits to Sustain Dividend Growth

Regarding its profitability, Altria is poised to report record adjusted EPS for Fiscal 2023. This suggests a continued commitment to its mission of consistently increasing its annual dividend. Let’s delve deeper.

Altria reported a significant increase in adjusted diluted earnings per share for the second quarter, rising by 4.0% to $1.31. This growth can be mainly attributed to a lower share count due to Altria’s share buybacks. Specifically, the company repurchased $1.21 billion worth of stock over the past four quarters, which equates to around 2.7% of Altia’s current market cap.

Based on the company’s half-year results, Altria’s management projects that adjusted diluted earnings per share will be between $4.89 and $5.03, suggesting an increase of 1% to 4% from Fiscal 2022’s result of $4.84. The midpoint of this range suggests that Altria is well-positioned to achieve another milestone in adjusted earnings per share, even in the face of the pessimistic sentiment shrouding its shares.

At this point, it’s important to mention that what should matter to you if you are an Atrlia investor is how much money ends up in the bottom line rather than the occasional revenue lag. This is because it’s the profits that directly affect whether Altria can keep returning tons of money to its investors in the future. That’s the main element that people who own shares in Altria should pay attention to since Altria’s entire investment case is built around the notion of its sky-high capital returns.

In that regard, following Altria’s most recent dividend increase, the annualized dividend rate of $3.92 is very well covered based on the midpoint of management’s EPS guidance ($4.96/share). It implies a healthy payout ratio of 79%, which should allow for further dividend hikes in the years to come. Coupled with the stock’s 9.0% dividend yield, Altria’s dividend prospects are hard to ignore.

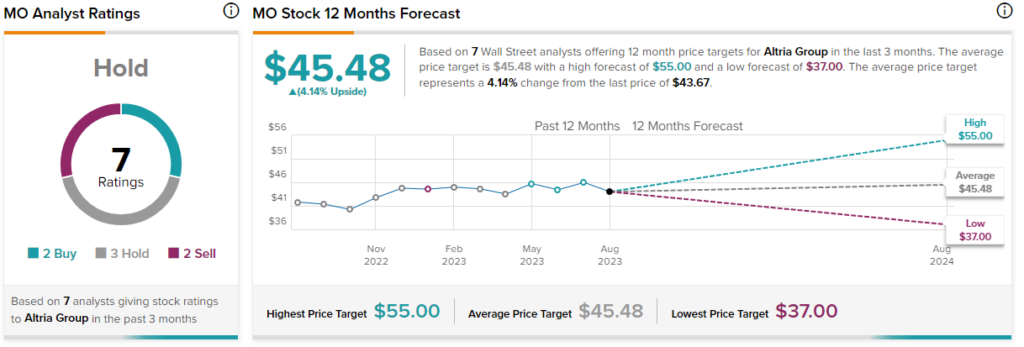

Is Altria Stock a Buy, According to Analysts?

Turning to Wall Street, Altria stock has a Moderate Buy consensus rating based on two Buys, three Holds, and two Sells assigned in the past three months. At $45.48, the average Altria stock price target implies 4.1% upside potential.

Final Thoughts

Altria’s unyielding commitment to dividend growth, exemplified by its 54th consecutive annual dividend increase, stands as a testament to its resiliency in a tough industry landscape. The tobacco giant’s ability to navigate through shifting market dynamics and deliver a robust financial performance underscores its capacity to generate substantial profits.

While acknowledging the evolving environment of smoking habits, Altria’s strategic focus on segments, like its booming Cigars division, can help sustain a cash-flow-rich future. Overall, as Altria forges ahead, its record profits should sustain further dividend growth, which makes for a compelling investment case, along with the stock’s already sky-high yield.